"Why Bio Spinoff IPOs Are So Prevalent"

등록 2025-06-25 오전 10:41:59

- [The Pharmaceutical Wealth of Nations, by Yoo Sung]

|

The comment captures why individual investors increasingly shun long-term bets in the sector, instead chasing risky short-term gains. According to President Jae-myung Lee, who visited the Korea Exchange on June 11, the root cause is structural.

“It’s no longer easy to invest long-term in quality stocks,” President Lee said. “Even if I invest in a company with solid fundamentals, it can suddenly become a shell through spinoffs or M&As.”

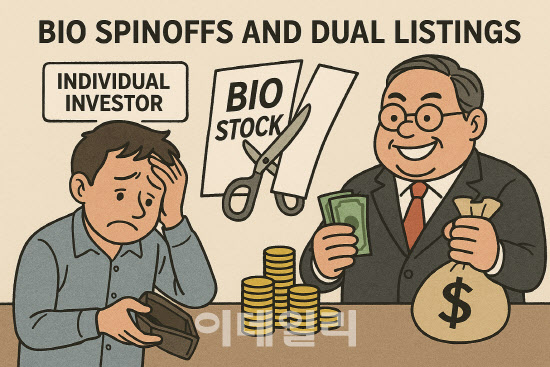

Lee’s remarks pointed squarely at the widespread practice of split listings and duplicate IPOs most prevalent in the biotech sector. Korean biopharma firms frequently spin off or separately list subsidiaries built around individual drug pipelines.

Such structural segmentation has become so normalized that even companies with annual revenues barely exceeding 1 trillion won (around $720 million) now control 20~30 subsidiaries. One pharmaceutical firm has more than 40. Considering that Korea’s entire pharmaceutical and biotech sector generates just around 30 trillion won comparable to a single conglomerate like CJ, this level of corporate fragmentation appears excessive.

The result is a dilution of revenue. Many of these firms report annual sales in the tens or hundreds of billions of won, at best. Even biotech startups with no revenue often operate three to four subsidiaries, underscoring how far the sector is from realizing economies of scale.

|

Recent examples of backlash include Oscotec, a biotech firm that attempted to list its subsidiary Genosco but withdrew after fierce opposition from retail investors. PharmaResearch, known for its skin booster brand Rejuran, also faced investor criticism after announcing plans to split into a holding company and a newly created entity to oversee its aesthetics business.

Retail investors are the biggest casualties of such fragmentation. While they buy into firms with growth potential, they often find themselves holding the hollowed-out remnants after value-driving assets are spun off. Meanwhile, controlling shareholders stand to gain the most from these maneuvers.

This market dynamic explains why retail investors resort to ultra-short-term biotech trading. However, President Lee’s public denunciation of split and duplicate listings has stirred hope that regulatory change may follow.

If new rules restrict such practices, analysts say, investors could regain confidence and shift toward mid- to long-term biotech investing. This, in turn, could reduce the extreme price volatility that currently characterizes Korea’s biotech capital markets.

K-Bio is already gaining momentum globally, buoyed by a string of successful license-out deals and drug development breakthroughs. Introducing systemic checks against exploitative listings could restore investor trust and further bolster the sector’s international standing.

To become a true global leader, K-Bio must strengthen not only its drug development pipeline but also its relationship with investors. Without their trust, even the most innovative firms risk losing their market foothold. In the end, short-term greed could lead to long-term failure.

저작권자 © 팜이데일리 - 기사 무단전재, 재배포시 법적인 처벌을 받을 수 있습니다.

류성 star@

함께보면 좋은 뉴스

![지놈앤컴퍼니, 임상 본격화 기대감에 급등…숨고르기 들어간 바이젠셀[바이오 맥짚기]](https://image.edaily.co.kr/images/vision/files/NP/S/2026/04/PS26043000447b.jpg)